FGF OP-ED

The Confederate Lawyer

May 12, 2016

Making and Destroying Money

by Charles G. Mills

fitzgerald griffin foundation

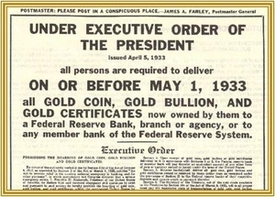

Executive Order by Franklin Delano Roosevelt

GLEN COVE, NY — The nations of the world in general, and America in particular, have destroyed real money by making so much of it that it has no permanent value.

When the United States adopted its Constitution, the new country's finances were in a terrible shape. Speculators were able to buy the paper promises of pensions made to veterans of the War of Independence for as little as a penny on the dollar. People whose wealth was in gold, silver, land, crops, and slaves despised those whose wealth was in paper promises, stocks, bonds, options, and other financial instruments. The only common currency was the “Continental,” which was essentially worthless. The new nation lacked a way to raise capital and a way to pay the war debts of the states.

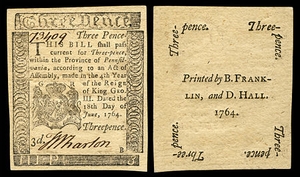

Continental currency from 1764

printed by Benjamin FranklinDuring the Washington administration, Secretary of the Treasury Alexander Hamilton laid the foundations of the modern American banking system by creating the concept of national banks and introducing the European concept of fractional reserve banking to America. Money was denominated in gold and silver. Paper money and deposits consisted of promises to pay gold or silver. A bank that created too much money in excess of its gold and silver reserves risked failing or having to be rescued by a larger bank on unfavorable terms. Some currency was issued as government notes, gold certificates, and silver certificates. Some was issued as notes of the First National Bank or the Second National Bank. Much was issued as bank notes of private banks.

At various times before the creation of the Federal Reserve System, there was a National Bank, one or more former National Banks that had become private, or both. During major wars, some paper money could not be redeemed for gold or silver until the wars ended.

In 1913, Congress enacted the system of Federal Reserve Banks as part of the national hysteria with progress. In some ways, the Federal Reserve Banks were like one more national bank, but gradually they became much more, as issuers of legal tender.

During the 1970s, all relationships between gold and silver, and paper money, bank deposits, and debts, were abolished. Today, all paper money consists of Federal Reserve notes.

Gold and silver are limited commodities, and thriving economies need more money than these limited commodities provide. One form of money consists of bank deposits. A person deposits gold or silver or paper money in a bank, and the bank promises gold or silver whenever the depositor wants it or writes a check against it. The deposit is a form of money with a specific gold or silver value.

Another form of money is paper money. In 1950, all paper money issued by a Federal Reserve Bank had a legend on it that it was redeemable in “real money," in theory initially gold or silver, and later silver dollars, half dollars, quarters, and dimes. The legend quietly disappeared in the 1960s as base metal quarters and dollars were introduced.

In 1933, the U. S. government required Americans to redeem all gold certificates and all gold coins, except small coin collections for paper money. During the 1970s, all relationships between gold and silver, on the one hand, and paper money, bank deposits, and debts, on the other hand, were abolished. Today, all paper money consists of Federal Reserve notes. The last major world leader who believed that money was not just a means of trade but also a means of storing value was Margaret Thatcher. All silver certificates and United States notes quietly disappeared at the end of the twentieth century.

The result of this has been constant inflation. This inflation has been much worse in actual costs than in exchange rates. Things that cost $.05 in 1950 now cost $2. Things that cost $.50 now cost $15. Things that cost $1,000 now cost $30,000. Experts may lie about the rate of inflation: it is clear, however, that in the past 75 years, the rate is actually 30-fold or higher.

The result of this has been constant inflation.

In the Hamilton model, if a national or private bank issued paper money, then invisible economic forces would keep the bank from issuing too much. If it issued too much, one of two things happened. People would withdraw so much gold and silver that the bank would fail, or a larger bank would lend enough gold or silver to keep the bank alive in exchange for a percentage of the bank's best assets. It is probably true that the Federal Reserve System did not create enough money in the 1920s, but the profit motive would have prevented this if the private banks had been the creators of money.

Today, the invisible hand of the free economy plays no role in determining the money supply. The Federal Reserve banks have a monopoly on issuing paper money and fixing bank reserves. The money supply is completely decided by the Federal Reserve Board that governs the Federal Reserve banks. The Federal Reserve Board has two goals. It lowers interest rates enough to keep the economy active and employment high by increasing the money supply. It also keeps interest rates high enough to keep inflation low by shrinking the money supply.

The system is out of control and allowing the Federal Reserve to finance a doubling of the national debt decade by decade.

This system has many flaws. All inflation is a form of theft. The professional economists employed by the Federal Reserve System can never come close to the invisible economic forces in accurately predicting inflation or recession. The Chairwoman of the Federal Reserve Board is in a state of confusion. The system is out of control and allowing the Federal Reserve to finance a doubling of the national debt decade by decade.

The present system encourages Congress to believe that it has an evergreen money tree and can spend an unlimited amount. It discourages simple saving and encourages speculation, or at least speculative guesses about future interest rates. It relieves the masters of the money supply of any consequences of their decisions.

We need to return to a system of permanent value for money and economic risk for those who expand or contract its supply.

###

The Confederate Lawyer archives

The Confederate Lawyer column is copyright © 2016 by Charles G. Mills and the Fitzgerald Griffin Foundation, www.fgfBooks.com. All rights reserved.

This column may be forwarded, posted, or published if credit is given to Charles Mills and fgfBooks.com.

Charles G. Mills Esq., is the Judge Advocate for the New York State American Legion. He has forty years of experience in many trial and appellate courts and has published articles on the law.

See his biographical sketch and additional columns here.

Help FGF to publish the Confederate Lawyer and other columns with a tax-deductible donation to:

Fitzgerald Griffin Foundation

344 Maple Avenue West, #281

Vienna, VA 22180

1-877-726-0058

publishing@fgfbooks.com

or donate online.

@ 2025 Fitzgerald Griffin Foundation